Nigeria’s external reserves have climbed above $50.11 billion, the highest level in seventeen years. The Central Bank of Nigeria confirmed the figure in early June 2026, marking a return to a level last seen in January 2009 when reserves stood at about $50.58 billion.

The milestone reflects relief for an economy that has faced sustained foreign exchange pressure, shaped by currency volatility, capital flow uncertainty, and repeated interventions to stabilise the naira.

The recovery is also evident in its pace. In June 2025, reserves stood at $38.28 billion. Within twelve months, Nigeria added roughly $11.83 billion, representing a year-on-year increase of about 30.9%. That makes it one of the strongest external balance improvements in recent years and points to improved FX inflows and market conditions. However, the numbers alone do not answer the central question of whether this is a structural shift or another temporary upswing.

For policymakers, the improvement is being interpreted as evidence that recent foreign exchange reforms are beginning to stabilise the system and attract inflows. For businesses and investors, it signals improved liquidity and a gradual easing of FX scarcity. But for analysts, the picture remains cautious, as the recovery is unfolding within an economy still exposed to oil dependence, volatile capital flows, and persistent import demand.

At the centre of the debate is a simple question. Can Nigeria sustain this momentum in a global environment shaped by volatile oil prices, shifting capital flows, and structural import dependence? The answer depends less on the headline figure and more on whether recent gains are anchored in durable reforms or still vulnerable to external conditions that can reverse quickly.

The drivers behind the rising reserves

Nigeria’s reserve accumulation over the past year has been driven by a mix of policy adjustments and improved foreign exchange inflows. Oil remains the most important factor. Crude production has improved modestly, rising to about 1.5 million barrels per day. This has strengthened export earnings and provided more consistent inflows into the external account. Even small gains in output translate into significant FX inflows due to the country’s dependence on hydrocarbons.

Diaspora remittances have also played a stabilising role. These inflows continue to provide a steady source of foreign currency and help cushion pressure on external buffers. Combined with improving investor sentiment, they have supported a gradual easing of strain in the FX market. Foreign portfolio inflows have also shown early signs of recovery, supported by higher yields and expectations of relative exchange rate stability, although flows remain uneven.

Monetary authorities have also leaned on a series of foreign exchange reforms aimed at improving transparency and reducing long-standing distortions in the market. The unification efforts and revised FX guidelines have helped narrow inefficiencies that previously discouraged inflows and encouraged arbitrage activity. Economists say this policy shift has been central to the recent improvement in external buffers, even if its long-term impact is still being tested.

According to Daniel John, a Lagos-based economist, the gains reflect both policy direction and cyclical support from oil earnings.

“Policy clarity has helped restore some confidence in the FX market, but reserves are still being supported by cyclical factors, especially oil-related inflows,” he told Businessfront. “The real test will be whether these inflows remain stable when global conditions tighten.”

Despite these improvements, John caution that portfolio inflows remain highly sensitive to global risk sentiment and can reverse quickly in response to external shocks or shifts in global interest rates.

How important Is the $50 billion milestone?

Crossing the $50 billion mark carries both symbolic and macroeconomic importance. It represents the strongest reserve level in seventeen years and a return to a key psychological threshold last seen before prolonged FX instability. In macroeconomic terms, reserves function as a buffer that supports imports, external debt obligations, and exchange rate management. When that buffer strengthens, it reduces immediate vulnerability to external shocks and improves market confidence.

The milestone also matters for how Nigeria is perceived internationally. Stronger reserves tend to ease pressure on the currency and improve investor sentiment. They also influence credit rating assessments, which closely track external buffers as indicators of macroeconomic stability.

According to John, the value of the milestone lies in the breathing space it creates for policy management.

“At above $50 billion, Nigeria has a stronger cushion to absorb external shocks and manage short-term FX pressures,” he said. “The real value is not just the size of the reserves, but the confidence it gives policymakers to avoid disruptive interventions in the foreign exchange market.”

Still, reserve adequacy depends on broader obligations such as import demand, capital outflows, and debt servicing. As a result, the milestone is a clear improvement in external strength, but not a complete guarantee of stability in a volatile global environment.

What’s different this time?

Nigeria’s current reserve build-up differs from previous cycles in both composition and policy context. Earlier episodes of reserve growth were driven largely by oil price booms that reversed quickly when global conditions shifted. This time, the increase reflects a broader mix of drivers, including FX reforms, modest oil production gains, and gradual return of portfolio inflows.

Policy reforms have also played a more visible role in shaping market behaviour. Adjustments to the FX framework have reduced distortions linked to multiple exchange rates and inefficient allocation. This has improved transparency and strengthened investor confidence, even if structural challenges remain.

Global conditions have also contributed. Higher global interest rates and shifting risk sentiment have encouraged selective inflows into emerging markets, including Nigeria. At the same time, diaspora remittances have provided a more stable inflow source compared to volatile capital flows.

Overall, what distinguishes this cycle is not the absence of risk, but the layering of multiple inflow sources and policy adjustments working in the same direction. However, oil remains the dominant driver, meaning structural vulnerability is still present.

What the $50 billion reserve mean for ordinary Nigerians

Nigeria’s $50.11 billion reserve position is an important macroeconomic milestone, but its impact on ordinary households remains indirect and uneven. The clearest transmission channel is inflation and exchange rate stability.

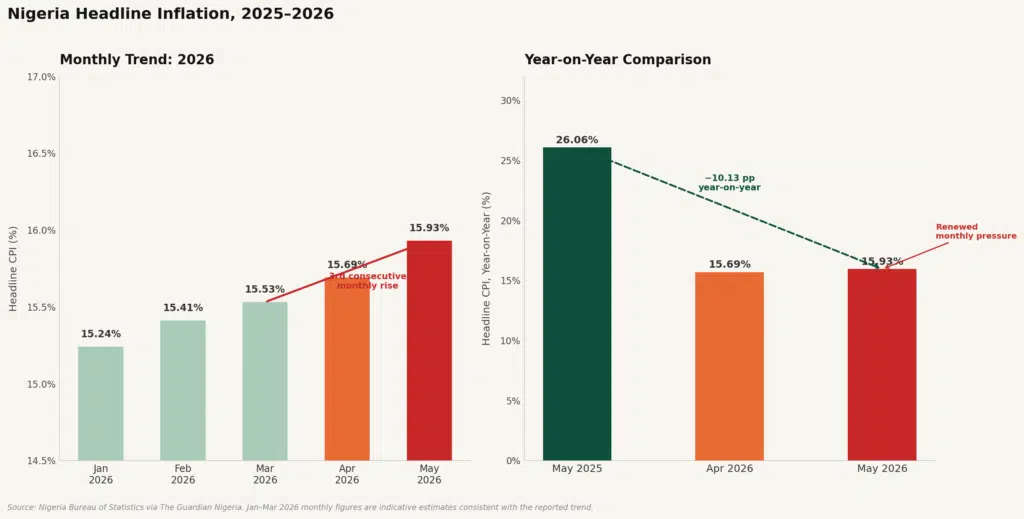

Nigeria’s headline inflation has maintained an upward swing in 2026, rising from 15.69% in April 2026 to 15.93% in May 2026. This marks the third consecutive month of sustained inflation increases within the year.

On a year-on-year basis, inflation stood at 15.93% in May 2026, compared to 15.69% in April 2026 and 26.06% in May 2025. While the year-on-year comparison shows moderation from 2025 levels, the recent monthly trend signals renewed price pressure in the economy.

Foreign exchange pressures remain a key driver of living costs in Nigeria. The economy still depends heavily on imports for fuel products, machinery, pharmaceuticals, and a wide range of consumer goods. This means reserve movements influence how stable the naira is in the foreign exchange market. When reserves are stronger, the Central Bank has more capacity to smooth volatility in the currency market, which helps reduce sudden spikes in import-driven costs.

However, the link between reserves and inflation remains indirect. Inflation is shaped by a mix of exchange rate movements, energy costs, transport expenses, and structural supply constraints. Even with stronger reserves, prices do not adjust downward quickly because many of the domestic cost pressures are persistent. What improved reserves can do is reduce the severity of currency instability, which helps slow the pace of imported inflation rather than reversing it.

The impact becomes more visible at the business level before it reaches households. Import-dependent firms experience relatively smoother access to foreign exchange when liquidity conditions improve, which helps stabilise supply chains and production planning. Over time, this can reduce the frequency of price shocks in consumer markets.

Still, energy costs, logistics inefficiencies, and weak domestic production capacity continue to exert upward pressure on prices. As a result, reserves act more as a stabiliser of volatility than a direct driver of improved purchasing power for households.

Structural weaknesses that could derail the recovery

Despite improved reserves, structural vulnerabilities remain significant. Oil still dominates export earnings, leaving reserves exposed to global price volatility and production disruptions. Even small shocks can quickly weaken inflows.

Import dependence also continues to pressure external buffers. Nigeria imports refined fuel, machinery, and pharmaceuticals, creating constant FX demand that offsets inflows. Debt servicing further tightens external conditions, with rising obligations consuming a growing share of FX earnings.

According to Yusuf Muinat, a financial analyst, Nigeria’s external position remains structurally exposed despite recent improvements.

“The reserve build-up is encouraging, but the economy is still vulnerable because it depends heavily on oil earnings and imports,” she told Businessfront. “Any sustained external shock can quickly weaken these gains if diversification does not improve.”

Overall, the improvement in reserves should therefore be seen as a strengthening of buffers rather than a resolution of structural weaknesses. The underlying drivers of vulnerability remain intact, meaning the recovery still depends heavily on external conditions rather than internal resilience.

Can this momentum last?

Nigeria’s current reserve build-up has created a sense of short-term stability, but the durability of this momentum remains uncertain. At over $50 billion, external buffers are stronger than in recent years, but sustainability depends on inflow quality rather than size.

Oil will remain the most decisive factor. Even with modest improvements in production, Nigeria’s fiscal and external accounts are still tied closely to global crude prices. A sustained downturn in oil prices or disruptions in output would immediately weaken FX inflows and slow reserve accumulation. This dependence means that external stability is still largely shaped by forces outside domestic control.

Global financial conditions also matter. Shifts in interest rates in advanced economies can quickly redirect capital away from emerging markets, including Nigeria. Portfolio inflows, which have supported recent improvements, remain particularly sensitive to these changes. At the same time, import demand continues to exert steady pressure on FX reserves, limiting how much of the inflows translate into net accumulation.

The more sustainable path would require stronger non-oil export growth, deeper industrial productivity, and reduced import dependence. Without these structural adjustments, reserve gains are likely to follow a cyclical pattern rather than a stable upward trend. In that sense, the current recovery reflects improved management of external inflows rather than a fundamental shift in the structure of the economy.

The momentum, therefore, is real but fragile. Nigeria has rebuilt its external buffers, but it has not yet insulated them from volatility. Whether this recovery lasts will depend on how quickly the economy can move from an oil-reliant inflow system to a more diversified and internally resilient export base.