Nigeria’s economy is, on paper, doing well. Tax collection is at record highs, oil revenue is surging, foreign reserves have crossed $50 billion for the first time in over a decade, and capital is flowing in from international investors at a pace not seen in recent memory.

By almost every headline fiscal metric, the government’s finances are in their strongest shape in a generation. Yet for the average Nigerian buying a bag of rice in Kano, paying annual rent in Lagos, or trying to keep a small business alive in Aba, none of this feels true.

Prices are still painfully high while wages have not kept pace, and the real value of what households can afford continues to shrink. This is the central paradox of Nigeria’s economy in 2025 and into 2026: the government’s coffer is getting fatter while the people’s pockets are getting leaner.

The reality lies in understanding how these contrasting trends are unfolding simultaneously, and why one has not yet improved the other.

The revenue machine is firing on all cylinders, with numbers backing it up

On all fronts and by most metrics, Nigeria seems to be in a relatively comfortable position when it comes to government reveue. Whether the consideration is taxes, petrodollar or foreign investments, the numbers all look good in paper.

For instance, Nigeria’s Federal Inland Revenue Service, the agency responsible for its tax revenue, collected about ₦22.59 trillion in taxes between January and September 2025, the highest total ever recorded for that period. In the first half of 2025 alone, tax revenue hit ₦14.27 trillion, a 43 percent increase from ₦9.98 trillion in the same period of 2024.

For context, total tax collection for the full first half of 2023 was just ₦5.5 trillion, meaning the government nearly tripled its tax haul in less than two years. The administration has pointed to this as vindication of its revenue reform agenda, and on the numbers alone, it is difficult to argue with that claim.

Earlier this year, the government introduced a new tax law aimed at boosting revenue collection. Among its key provisions is an increase in the capital gains tax rate from 10% to 30%. Experts say the broader tax reforms could significantly expand the government’s revenue base, with some projections suggesting collections could double within the next two years.

Similarly, oil revenue tells a familiar story. Nigeria earned ₦55.5 trillion from crude oil sales across the full year of 2025, acoording to reports.

The Nigerian National Petroleum Company (NNPC), the state-owned oil firm, remitted over ₦14.7 trillion to the Federation Account during the year. In addition, crude output hit a five-year high of 1.71 million barrels per day between April 2025 and April 2026, a recovery that reflects genuine progress in tackling oil theft, pipeline vandalism and the production disruptions that bled the country throughout the late Buhari years. For a government that came into office promising to fix the oil sector, this is a tangible result.

On the reserves front, the Central Bank of Nigeria (CBN) reported gross external reserves of $50.04 billion as of June 2026, the highest level in 13 years. When one also considers the net reserves, which strip out short-term liabilities and give a cleaner picture of what the country actually earns, the number has climbed from just $3.99 billion at the end of 2023 to $34.80 billion by the close of 2025, the CBN’s chief, Yemi Cardoso, said in a recent statement.

That is an increase of more than 770 percent in two years. Cardoso has cited repeatedly this number as evidence of the central bank’s reform programme working. Apart from its reserve, Nigeria’s capital inflows completed the picture, with total capital importation reaching $23.21 billion in 2025, up 88.5 percent from the year before, and rising further still to $10.37 billion in just the first quarter of 2026.

Taken together, these numbers describe a government whose fiscal position has transformed remarkably in a short period. They also set up a question that the numbers themselves cannot answer: where is any of this going?

What is driving the revenue boom:

| Revenue Source | 2023 | 2025 | Change |

|---|---|---|---|

| FIRS Tax Revenue (H1) | ₦5.5 trillion | ₦14.27 trillion | +159% |

| NNPC Federation Remittance | ₦6 trillion | ₦14.7 trillion | +145% |

| CBN Net Reserves (year-end) | $3.99 billion | $34.80 billion | +772% |

| Total Capital Importation | $6 billion | $23.21 billion | +88.5% |

Why the numbers feel like a lie for ordinary Nigerians

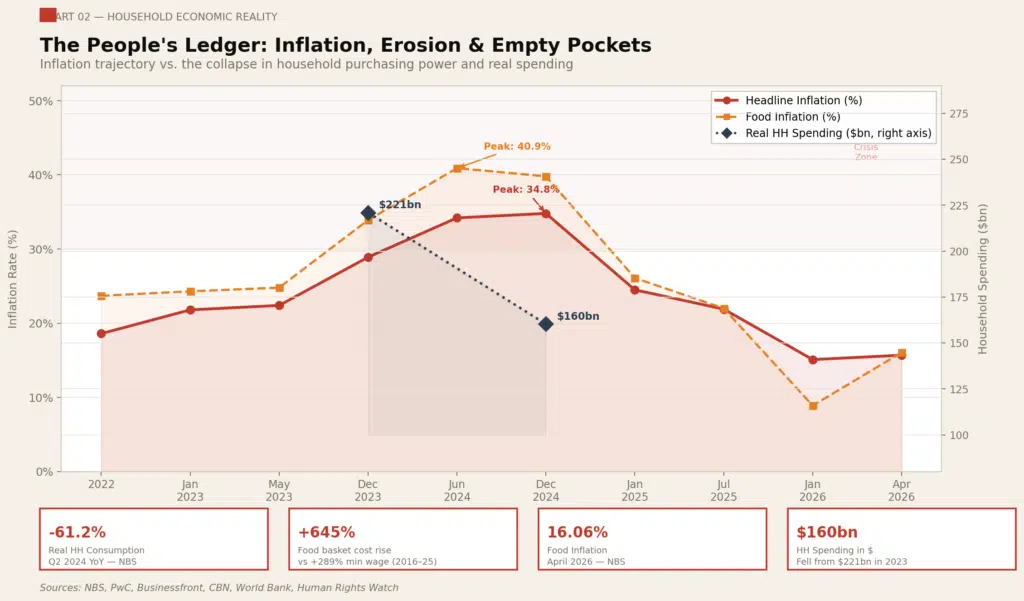

While the government’s ledger has improved dramatically, the household ledger has moved in the opposite direction with equal force.

Nigeria’s real household consumption expenditure fell by 42.28 percent in the first quarter of 2024 on a year-on-year basis and then collapsed by 61.18 percent in the second quarter, according to the National Bureau of Statistics (NBS). These are not small statistical fluctuations. They represent a profound contraction in what Nigerian families could actually afford to buy in real terms, after accounting for the inflation that had been eroding naira incomes since the fuel subsidy removal and currency float of mid-2023.

Nominal household spending did grow, rising from ₦142.6 trillion in 2023 to ₦237 trillion in 2024. But in dollar terms, the more honest measure of purchasing value, total household spending fell sharply from $221 billion to $160.3 billion in that period. Nigerians were spending more naira to buy less.

PwC, a global consulting firm which tracked this trend closely, attributed the nominal expansion almost entirely to surging food prices and higher transport costs rather than any genuine improvement in household income or wealth.

The picture is even more bleak when we consider what this looks like outside of a spreadsheet.

In Lagos, the nation’s commericial centre, annual rent for a standard two-bedroom flat now runs between ₦1.5 million and ₦4 million, with total move-in costs rising to between ₦2.5 million and ₦6 million once agent fees, caution deposits and legal charges are added. Against a national minimum wage of ₦70,000 per month, that means a minimum-wage earner would need to save every kobo of their income for between three and seven years just to afford to move into a standard flat. Civil servants with fixed salaries are increasingly relocating to distant suburbs and commuting for hours, not because they prefer it but because that is the only way to keep shelter and food in the same budget.

One civil servant interviewed by The Guardian newspaper captured the logic plainly: “We are choosing between feeding our families properly and keeping the roof we already have.” That is not the language of a population experiencing an economic boom.

Small business operators are faring no better. A cold-room business in Ikeja now spends ₦400,000 monthly on diesel alone, a figure that in many cases exceeds the business’s rent. Electricity remains the highest operating cost for most Nigerian SMEs, followed by rent and the cost of capital, three costs that have all risen sharply since 2023.

Market traders who sell food staples report that the price of inputs rises with almost every restock and that customers who once bought in bulk now buy smaller quantities, or stop buying certain items altogether. The result is that even when a business is technically operational, its revenue base is shrinking beneath it. Over 95 percent of Nigerian SMEs fail within five years, and the environment since 2023 has made that statistic harder, not easier, to escape.

The food price data captures the scale of the damage most directly. A basic food basket containing rice, beans, garri, bread, eggs and yams that cost roughly ₦13,000 in 2016 now costs close to ₦97,000. That is a 645 percent increase in the cost of feeding a household over nine years, against a minimum wage that rose by 289 percent over the same period. Imported rice alone went from around ₦239 per kilogram in early 2016 to more than ₦2,255 by late 2025, an increase of over 800 percent. The cost of cooking one pot of jollof rice, a cultural and dietary staple in millions of Nigerian homes, jumped to ₦25,486 by March 2025, up from ₦21,300 just six months earlier, a 19 percent spike in the price of a single meal.

The World Bank estimated Nigeria’s poverty rate at 63 percent in 2025, meaning roughly two in every three Nigerians are living below a meaningful income threshold even as the government posts its most impressive fiscal numbers in a decade. Nigeria’s per capita income fell to an estimated $835 in 2025, placing it among the lowest in its peer group of major African economies.

Two Nigerias: Government revenue vs. household reality:

| Indicator | Government Side | Household Side |

|---|---|---|

| Revenue | ₦22.6tn tax collected Jan–Sep 2025 | Real consumption fell 61% in Q2 2024 |

| Reserves | $50bn gross reserves, Jun 2026 | HH spending fell from $221bn to $160bn |

| Capital inflows | $23.21bn in 2025, +88.5% | FDI just 1.3% of Q1 2026 inflows |

| Oil | ₦55.5tn crude revenue in 2025 | Fuel price rose by 463% in 3 years |

| Poverty | — | World Bank: 63% poverty rate (2025) |

What is making the government rich is keeping ordinary people poor

The glaring paradox between what the government is earning and what Nigerians are left with is by n means a coincidence. It is not simply the story of a government that has been slow to share the benefits of growth. In actual fact, the forces driving the revenue boom are, in several direct and measurable ways, the same forces straining household budgets. Understanding that connection is what separates a fiscal headline from an economic reality, and it explains why record government earnings can coexist with record household suffering.

When global oil prices rise, Nigeria earns more from crude exports and government revenue climbs. But because Nigeria still imports most of its refined petroleum products and even crude oil despite having a working refinery, higher global oil prices also push up the domestic cost of fuel, cooking gas, transport and electricity generation. The benefit of higher oil prices flows upward into government accounts and NNPC’s balance sheet. The cost flows downward, into the operating expenses of every business that runs a generator, every person who pays a bus fare, and every household that buys kerosene or gas to cook.

With fuel subsidies now removed, these higher global prices are passed through more directly to consumers. In the past, the government absorbed part of the increase to keep pump prices lower. Today, households and businesses bear much more of the cost, making them more vulnerable to swings in international energy markets.

The price of energy is one of the most regressive costs in any economy because it takes a larger proportional share from people at the bottom of the income scale than from those at the top.

In addition, tax collection and reforms have been effective in building a strong revenue base for the government, but it is not neutral in how its costs are distributed. The compliance burden, higher corporate levies and tighter enforcement on large businesses translate directly into higher costs of doing business, and those costs do not stay with the companies that pay them. They move into the prices of goods and services that ordinary Nigerians pay every day.

A manufacturing firm facing a larger tax bill, higher energy costs and tighter import regulations does not absorb those costs quietly. It raises prices. A small distributor buying from that manufacturer raises prices again. By the time a product reaches a market stall or a corner shop, the cost of Nigeria’s tax and regulatory environment is embedded in its price tag, and the person paying it is someone whose income has not changed.

The capital inflows story is equally complicated when examined more closely. Reserves crossing $50 billion is a genuine achievement, and the CBN is right to point to it as a sign of improving external sector health. But of Nigeria’s $23.21 billion in capital importation in 2025, portfolio investment accounted for more than 85 percent of the total.

In the first quarter of 2026, that figure rose further to 95.1 percent, with foreign direct investment making up just 1.3 percent of total inflows. What Nigeria is attracting is overwhelmingly portfolio capital, money that comes quickly in search of high yields from treasury bills and bonds, and leaves just as fast when global interest rates shift or investor sentiment changes. This type of capital does not build factories, does not employ workers at scale and does not raise wages. The CBN also deliberately manages how much of this liquidity it releases into the broader economy as part of its inflation control strategy, which means strong reserve figures and tight consumer money supply exist simultaneously and by design.

Then there is the debt burden, which sits at the structural core of why record revenue years still leave public services underfunded and ordinary Nigerians without visible benefit.

Between January and September 2025, Nigeria spent ₦12.63 trillion on debt servicing, more than four times the ₦3.1 trillion released for capital and infrastructure development in the same period. The 2025 budget allocated ₦15.4 trillion to debt servicing, while education received ₦3.52 trillion and health received ₦2.48 trillion. Education sits at 7 percent of the total budget.

Olawole Isaac, an investment banker and economist based in Abuja, told Businessfront that Nigeria’s rising debt service burden is not only unsustainable but also at odds with the goal of maintaining healthy public finances, particularly in critical sectors such as infrastructure and education.

“Nigeria’s debt servicing continues to grow despite the removal of policy buffers like fuel subsidies and the naira defence. What this shows is a system that struggles with accurate planning and project financing, because once the bills are paid, there is little left for anything else,” Isaac said.

A government earning record revenues but committing the majority of those earnings to debt repayment is a government that cannot translate fiscal strength into better lives for the people it governs. The money is coming in. It is just not staying in the country in a form that reaches households.

Whether this changes depends on decisions that have not yet been made

There are genuine signs that the worst of the price pressure has passed, and they deserve to be acknowledged honestly. Headline inflation fell from its 2024 peak of nearly 35 percent to 15.69 percent by April 2026. Food inflation briefly hit a 10-year low of 8.89 percent in January 2026, the first single-digit reading since May 2015, before ticking back up to 16.06 percent in April as seasonal and structural pressures reasserted themselves. Prices of key staples including rice, beans and garri have fallen year-on-year from their 2024 peaks. The naira has stabilised. Crude output is at a five-year high, which strengthens the external position.

On each of these measures, the direction of travel is better than it was a year ago, and that matters. Nigerians living through this period know the difference between things getting worse and things getting less bad, even if less bad still falls well short of good.

But specific structural concerns remain, and they are serious enough to temper any optimism. The IMF revised its per capita income forecast for Nigeria downward in April 2026 to $804.5, lower than an earlier estimate of $940.2, which means the multilateral consensus on Nigerian household income is moving in the wrong direction even as the government’s fiscal numbers improve.

More than 80 percent of households surveyed by the CBN in its inflation expectations report said they believed prices would remain elevated, a signal that the psychological damage of the inflation years is not easily erased by a few months of moderation and that consumer confidence remains fragile. Rural inflation remains higher than urban inflation at 16.36 percent versus 15.40 percent in April 2026, meaning those with the fewest economic buffers are still bearing the most pressure. Nigeria’s public debt reached 52.3 percent of GDP in 2024, up from 41.5 percent in 2023, driven partly by a weaker naira inflating the naira value of external obligations, and the trajectory of that ratio matters for how much fiscal space the government has in future years to spend on people rather than creditors.

The dominance of portfolio investment over foreign direct investment also represents an unresolved vulnerability. Until the capital flows that are building reserves begin shifting toward productive investment in manufacturing, agriculture and infrastructure, the macroeconomic improvements will remain largely invisible to the majority of Nigerians. A country can have strong reserves and a weak economy for its citizens at the same time. Nigeria is currently demonstrating that this is possible.

Lastly, Nigeria’s fiscal architecture is, without question, stronger than it has been in years. The government has more money, more reserves and more policy tools than it did when the current administration took office. Whether that strength eventually reaches households will be shaped by decisions still ahead. These include how the debt burden is managed and reduced over time. It also involves how the tax system is designed so businesses can absorb compliance costs without fully passing them on to consumers.

Another factor is whether investment conditions improve enough to attract foreign capital that creates jobs rather than short-term yield-seeking inflows. It will also be determined by whether budget allocations to health, education, and infrastructure begin to reflect the scale of need rather than what remains after debt service is paid.

The revenue boom is real. So is the suffering of ordinary Nigerians. Bridging the distance between those two realities is the unfinished work of Nigeria’s economic reform, and the urgency of that work does not diminish with each new revenue record.