Africa’s solar expansion is accelerating at a pace that would have been difficult to imagine a decade ago. Across Nigeria, South Africa, Kenya, Egypt, Morocco, and other African countries, solar power is no longer positioned as a backup option. It is increasingly becoming a central pillar of energy supply for households, businesses, and industrial users.

This shift is driven by persistent grid instability, rising electricity tariffs, and the growing cost of diesel-based self-generation across many African economies. Solar growth is not being driven by policy ambition alone. It is being shaped by necessity, as grid reliability remains inconsistent.

At the centre of this transformation sits China. The country has become the dominant supplier of solar panels, inverters, and related components across global markets, including Africa. Its manufacturing capacity, scale efficiencies, and long-standing industrial policy support have made it the anchor of the global solar supply chain.

However, this rapid expansion raises a more complex question about dependency and transition. While solar adoption is increasing across the continent, the supply chains that enable this growth remain heavily concentrated outside Africa. The same Chinese manufacturing dominance that made solar affordable is also shaping how African countries access energy infrastructure today.

This creates a structural tension between rapid energy access and long-term industrial independence. It is within this context that the question emerges: is the era of cheap Chinese solar imports in Africa approaching an end, or is it simply evolving into a more strategic phase?

The answer is not straightforward. What is clear, however, is that the structure of the global solar market is shifting, and Africa is being pulled into that change.

How China built the “cheap solar” era

China’s dominance in solar energy did not emerge from market chance. It was the result of more than a decade of coordinated industrial strategy backed by state policy, financing support, and large-scale manufacturing expansion. By the early 2010s, China had already begun consolidating control over the global photovoltaic value chain, particularly in polysilicon, wafers, solar cells, and finished modules.

Today, it accounts for more than 80 percent of global solar module production capacity. This level of concentration has allowed China to influence global pricing structures in ways no other country can match. The result has been a sustained downward pressure on solar equipment costs across global markets, including Africa.

The “cheap solar” era was largely built on scale economics and aggressive capacity expansion. Chinese manufacturers expanded production far beyond domestic demand, creating global oversupply conditions that pushed module prices down over the past decade.

This price collapse fundamentally changed the economics of solar energy in emerging markets. Countries across Africa became major import destinations because solar suddenly became cheaper than diesel-based self-generation in many use cases. This triggered rapid adoption, particularly in distributed and off-grid systems where upfront cost sensitivity is highest.

Most solar imports into African markets flow through a layered distribution chain involving Chinese manufacturers, global trading hubs, and regional importers. This structure allowed African countries to access low-cost solar technology without building domestic manufacturing capacity.

However, it also created structural dependency on external supply chains. The affordability of solar energy in Africa is therefore not just a result of technological progress, but also a reflection of China’s ability to sustain global overcapacity in manufacturing for an extended period.

Why prices are collapsing globally

The global decline in solar prices has been driven mainly by sustained overcapacity in manufacturing, particularly in China. Over the past decade, production of solar modules expanded faster than global demand, creating intense competition among manufacturers. This led to aggressive price reductions as firms prioritised volume over margins.

Solar module prices have fallen by more than 90 percent over the last decade. This price decline is now beginning to stabilise. Chinese manufacturers are shifting away from pure price competition as profit pressures increase and industry consolidation intensifies. Several producers are slowing capacity expansion and focusing more on efficiency and supply chain control. As oversupply eases, the extreme downward pressure that defined the “cheap solar era” is weakening. This signals a transition from a prolonged price collapse to a more structured and stable pricing environment.

Trade and logistics pressures are reinforcing this shift. Tariffs in major markets and global shipping volatility have increased landed costs for exporters. These factors have slowed the pace of price reductions, even though solar remains one of the cheapest sources of electricity generation globally.

In Africa, this is beginning to influence purchasing decisions, with buyers placing more weight on financing terms, system reliability, and long-term performance rather than upfront cost alone.

Khalid Adeleke, a Lagos-based solar energy and sustainability researcher, told Businessfront that the global solar market is moving out of its ultra-low-cost phase.

“The period of aggressively cheap Chinese solar exports was driven by overcapacity and intense price competition. That phase is now stabilising. What we are seeing is not the end of Chinese dominance, but the end of structurally falling prices that defined the last decade,” Adeleke said.

He added that Africa’s dependence on Chinese imports is unlikely to disappear in the short term, even as pricing dynamics evolve. According to him, the key change is that solar supply is becoming more strategically managed rather than purely export-driven.

Africa’s solar demand is changing

Africa’s solar market is no longer driven mainly by early adoption or basic electrification. It is increasingly shaped by businesses and industries responding to unreliable grids and rising energy costs. Solar is now treated as essential infrastructure for keeping operations running rather than an optional energy sources. This shift matters because it is changing what the market demands from suppliers, not just how much it consumes. The focus is moving from low-cost imports to reliability, scale, and long-term performance.

This change is also reshaping procurement patterns. Household systems, which once dominated imports, are gradually being overtaken by commercial and industrial installations. These systems require more advanced equipment, structured financing, and stronger technical support. Buyers are increasingly evaluating total system value rather than just upfront cost. This is the first clear pressure point on the “cheap import model”, even if it still dominates overall supply.

At the same time, Africa’s energy gap continues to accelerate demand. The continent holds around 60 percent of the world’s best solar resources, yet solar accounts for only about 3 percent of total electricity generation. This gap reflects both low penetration and high growth potential, especially in markets where grid failure directly affects economic output. It also explains why demand is rising in concentrated bursts rather than evenly across the continent.

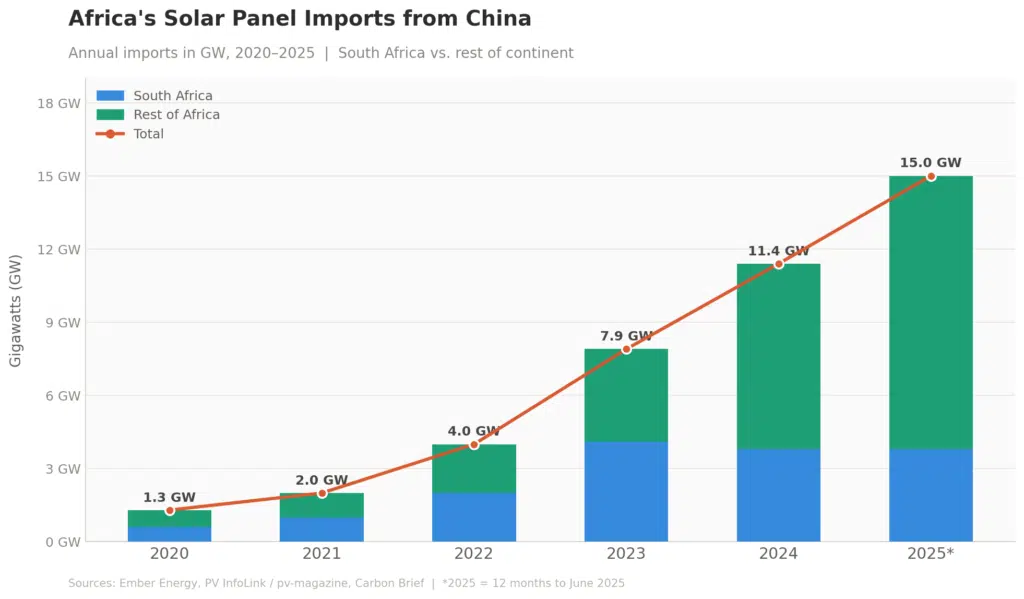

In 2025, Nigeria installed about 803 megawatts of solar capacity, making it the second-largest installer in Africa after South Africa, which added around 1,602 megawatts.

These figures show that demand is no longer experimental but increasingly tied to core economic activity. However, most of this equipment is still imported, largely from China, meaning demand is changing faster than the supply structure behind it.

Rising localisation across African markets

Across several African markets, governments are increasing efforts to build local participation in renewable energy value chains. This is driven by energy security concerns, pressure on foreign exchange, and the need to retain more value from rising solar demand. Countries such as South Africa, Nigeria, and Kenya have introduced policies supporting local assembly and domestic involvement in renewable energy projects.

However, these efforts are unfolding in economies still heavily dependent on imported solar technology. The result is a gradual move towards localisation, but not a break from import reliance.

The main constraint remains upstream manufacturing. Africa still depends on external suppliers, especially China, for key components such as polysilicon, wafers, and solar cells. Most local activity is therefore limited to assembly, installation, and distribution rather than full production. Even where local content rules exist, they are constrained by cost pressures and weak industrial capacity. This makes localisation more about partial value capture than true supply chain independence.

Large-scale projects show both progress and limitation. In Egypt, the Benban Solar Park is one of the world’s largest photovoltaic installations, with a capacity of about 1,650 megawatts and annual output of roughly 3.8 terawatt-hours. It highlights Africa’s ability to attract major international solar investment at scale.

In Morocco, the Noor Ouarzazate Solar Complex combines concentrated solar power with hybrid systems, including auxiliary diesel generation, to stabilise output. Both projects demonstrate strong infrastructure ambition, but also continued reliance on imported technology and external engineering expertise.

Localisation in Africa is currently an infrastructure and assembly story, not a manufacturing shift. While large projects are expanding solar capacity, they are still deeply tied to external supply chains, particularly from China. Instead of reducing imports, these developments are reshaping how imports are deployed in larger and more complex energy systems. This reinforces the central tension in Africa’s solar transition between rising ambition and persistent external dependence.

Emerging competitors and diversification attempts

Despite China’s dominance in Africa’s solar supply chain, there are early signs of diversification in global supply routes. India has begun expanding its solar manufacturing capacity through state-backed industrial programmes, positioning itself as a potential alternative exporter to emerging markets.

Turkey and several Southeast Asian economies, including Vietnam, Malaysia, and Thailand, are also increasing their presence in Africa’s renewable energy supply chain. However, despite this diversification, these players remain significantly behind China in scale, cost efficiency, and vertical integration. Their participation is expanding access and choice for African buyers, but it has not yet altered the structure of global solar dominance.

Within Africa itself, there are also early attempts to build domestic manufacturing capacity. In September of last year, Nigeria announced plans to develop a 1 gigawatt solar panel manufacturing factory. The project signals a shift towards industrial-scale renewable energy production and reflects a broader ambition to position the country as a regional hub for solar equipment manufacturing.

If implemented successfully, it could reduce reliance on imports in the long term and strengthen local value chains. However, like similar initiatives across the continent, its success will depend on financing, infrastructure, and consistent policy support.

Despite these developments, the current competitive landscape remains heavily skewed. China continues to dominate upstream manufacturing, controlling key inputs such as polysilicon, wafers, and solar cells. This gives Chinese firms a structural advantage that emerging competitors have not yet matched. As a result, diversification is occurring at the margins rather than as a full-scale shift in supply dominance. Most African solar imports still originate from China, either directly or through intermediary trading hubs.

The implication is that competition is growing, but not yet disruptive. Emerging players are expanding options for African buyers, but they are not replacing China’s central role in the global solar ecosystem. Instead, they are gradually adding layers of complexity to a market that remains structurally dependent on Chinese manufacturing capacity.

Why Africa’s solar growth may still rely on China

Africa’s solar market is expanding at its fastest pace in years, but its underlying structure remains heavily dependent on external supply chains. In 2025, Africa emerged as the world’s fastest growing solar market, with installed capacity rising by 17%, driven largely by imports of Chinese-made solar panels. This growth is taking place within a broader global expansion, with solar capacity increasing by 23 percent to 618 GW, although momentum has slowed from a 44% increase in 2024.

This dependency is reinforced by trade flows. China’s exports of solar cells and panels to African countries surged by 83 percent year-on-year in April this year, reaching 123,787 metric tons, up from 67,552 tons a year earlier. Although shipments eased from March’s record level, analysts note that underlying demand remains strong. This shows that Africa’s solar expansion is still being absorbed primarily by Chinese manufacturing output rather than alternative suppliers or domestic production.

The scale of unmet demand continues to define the region’s energy landscape. According to the International Energy Agency, nearly 600 million people across Africa still lack access to electricity, while many more experience unreliable supply even where grid connections exist. This structural deficit is increasingly being addressed through solar deployment, particularly in off-grid and commercial applications.

However, the equipment enabling this transition is still predominantly imported, with China maintaining dominance across key components such as modules, inverters, and upstream materials. This ensures that even locally deployed systems are anchored in external supply chains.

In practical terms, Africa’s solar boom is accelerating, but it remains structurally tied to Chinese manufacturing capacity. Until local manufacturing or diversified global supply chains reach meaningful scale, China will remain central to how this expansion is delivered and sustained. The result is not a weakening of dependency, but a scaling of it alongside rising demand.

Is this the end of Chinese solar imports in Africa?

The era of cheap Chinese solar imports in Africa is not ending, but it is evolving into a more structured and strategically embedded system. Across the continent, solar demand is expanding rapidly, but supply chains remain heavily concentrated in China. Even as pricing stabilises and procurement becomes more sophisticated, China continues to dominate upstream manufacturing. This keeps Africa’s solar expansion anchored to Chinese industrial capacity rather than a diversified global production base.

“What we are seeing is not a break from Chinese solar dominance, but a reconfiguration of it. China is moving from purely low-cost exports to a more integrated supply and infrastructure model, while Africa’s demand is scaling faster than its ability to localise production,” Adeleke said.

The market is moving away from ultra-low-cost exports toward a system where Chinese firms are embedding themselves in long-term energy infrastructure development. This includes overseas assembly, financing-linked supply contracts, and integrated project delivery. African markets are also evolving in their demand structure, but not yet in their production capability. As a result, the system is becoming more complex, not less dependent.

The conclusion is therefore straightforward. Africa’s solar expansion is not moving away from China. It is scaling through it. The real story is not the end of cheap Chinese solar. It is the transformation of how China participates in Africa’s energy future. The “cheap solar import era” is not ending in Africa. It is transitioning into a more stable but deeply embedded phase of dependence.