South Africa’s local currency, the rand, weakened in early trade on Monday as global financial markets reacted to rising oil prices and renewed geopolitical tensions in the Middle East.

The rand traded at 16.6050 against the US dollar, marking a decline of about 0.5 percent from its previous close. The move reflected a broader shift in global risk sentiment that continues to weigh on emerging-market currencies. The pressure on the rand is not coming from a single domestic trigger. Instead, it reflects a wider global adjustment driven by stronger US economic data, rising energy prices, and elevated geopolitical uncertainty.

These forces are reshaping expectations across currency, commodity, and bond markets at the same time. South African financial markets also showed early signs of strain, with equities and government bonds moving lower in line with global trends.

The moves were not extreme, but they point to a coordinated risk-off environment that is becoming more visible across emerging economies.

While these figures reflect typical risk-off trading conditions, the combination of a weaker rand and rising oil prices raises deeper concerns for South Africa’s economy. The country remains highly exposed to global energy price movements due to its reliance on imported fuel and sensitivity to external capital flows. The key issue is not only why the rand is weakening, but what rising oil prices mean for inflation, growth, and financial stability.

Understanding why the rand is under pressure

The rand weakened against the US dollar, representing a 0.5% decline in early trade. The move came as the US dollar strengthened to a two-month high following stronger-than-expected US employment data. This reinforced expectations that the US Federal Reserve may maintain higher interest rates for longer.

Higher US interest rates matter for emerging markets because they reshape global capital flows. When US yields rise, investors tend to move funds into dollar-denominated assets that offer higher returns and lower risk. This reduces capital inflows into emerging markets such as South Africa, which rely on foreign investment to support currency stability.

At the same time, Brent crude oil prices rose by more than $4 per barrel during the session. The increase was driven by renewed geopolitical tensions in the Middle East, raising concerns about potential supply disruptions. Oil markets tend to react quickly to geopolitical risk because supply chains depend heavily on stability in key producing regions.

When oil prices rise while the US dollar strengthens, emerging-market currencies come under double pressure.

The dollar attracts capital inflows while oil increases inflation risk globally. South Africa is particularly sensitive to this combination because of its dependence on imported energy and foreign capital inflows. The result is a feedback loop where external shocks translate quickly into currency weakness.

South Africa’s structural dependence on imported oil

Meanwhile, South Africa remains heavily dependent on imported crude oil and refined petroleum products. Domestic production is not sufficient to meet national demand, which makes the country reliant on international supply chains for energy security.

Because oil is priced in US dollars, exchange rate movements directly influence domestic fuel costs. When the rand weakens, imported fuel becomes more expensive even if global oil prices remain unchanged. When both factors move together, the impact is significantly amplified.

This dependence means South Africa is exposed to global energy cycles in a direct and immediate way. Unlike oil-producing economies, it does not benefit from higher global prices. Instead, it absorbs higher import costs that feed into transport, logistics, manufacturing, and broader production expenses.

Fuel is a core input across the economy. It powers transportation systems, industrial production, mining operations, and agricultural activity. As a result, oil price movements do not remain confined to energy markets. They quickly transmit into inflation trends, business costs, and household spending patterns.

Economists say this structure leaves South Africa highly exposed to global shocks, especially when currency weakness and oil price increases occur at the same time.

According to energy economist Sarah Mokoena, the issue is less about fuel consumption and more about how external pricing flows into the domestic economy.

“South Africa imports both oil and the currency risk attached to it. Any movement in the dollar or crude prices is immediately reflected in local fuel costs,” she told Businessfront. “When the rand weakens at the same time as oil prices rise, the impact is not linear. It compounds.

Meanwhile, South Africa’s National Treasury said it still expects government debt to stabilise as projected, despite higher oil prices and market volatility stemming from the conflict in the Middle East.

The Treasury noted that stronger commodity export prices could help cushion the impact of rising oil costs on the rand.

Why rising oil prices hit South Africa harder than most economies

The impact of rising oil prices in South Africa is intensified by the interaction between currency weakness and import dependence. When oil prices rise in dollar terms, import costs increase immediately. When the rand weakens at the same time, the cost impact multiplies. This creates a double shock effect where the same barrel of oil becomes more expensive due to both global price increases and exchange rate depreciation.

The economy is also heavily dependent on fuel-intensive sectors. Transport and logistics form the backbone of domestic distribution networks. Agriculture relies on fuel for machinery and irrigation. Mining and manufacturing require significant energy inputs to sustain production. Because these sectors account for a large share of economic activity, oil price movements quickly spread across the broader economy.

Even small changes in global energy prices can therefore have large domestic effects. Small and medium-sized enterprises are also exposed through rising transport costs, and many operate on thin margins, making them particularly vulnerable.

Could higher oil prices reignite inflation?

Inflation in South Africa is closely tied to fuel price movements because transport costs sit at the centre of the consumer basket. When oil prices rise, domestic fuel prices adjust quickly, feeding into logistics, food distribution, and retail pricing. This creates one of the fastest transmission channels from global markets into household inflation.

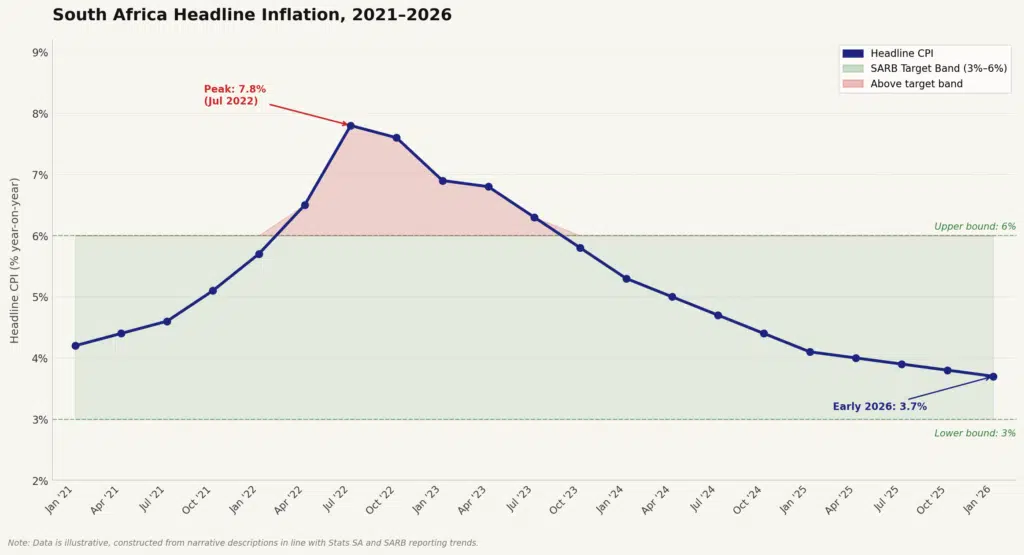

South Africa’s inflation experience over recent years has been shaped by global shocks rather than a steady trend. Headline inflation moved above the South African Reserve Bank’s 3%–6% target band in 2022. It remained elevated through parts of 2023 before easing through 2024 as global energy and food prices stabilised.

By 2025, inflation had largely moderated back within the target range. Recent readings into early 2026 have generally remained within or close to the lower half of the target band, according to Stats SA releases and central bank tracking.

The South African Reserve Bank has said it expects headline inflation to be higher in the near term, averaging about 3.7 percent this year, before easing back toward its target range by late 2027. The projection reflects lingering risks from energy prices and exchange rate volatility, even as broader inflation pressures have cooled.

This moderation does not remove underlying vulnerability. Inflation remains highly responsive to external shocks, particularly fuel and food prices. The shift from high inflation in 2022–2023 to lower readings in 2024–2026 reflects cyclical easing rather than a structural break in sensitivity.

Food inflation remains highly sensitive to fuel costs. Agriculture and food distribution depend on transport and energy inputs. As a result, higher oil prices tend to feed into food prices with a short lag. Transport inflation is another key channel. Fuel is a major input cost for logistics operators and public transport systems. When fuel prices rise, freight costs adjust quickly and are passed through the supply chain over time.

Although inflation has recently moderated, imported inflation remains a key risk. A weaker rand combined with higher oil prices increases the likelihood of renewed inflation pressure. This matters for monetary policy. The South African Reserve Bank closely monitors inflation expectations. If oil-driven inflation rises again, it could delay the timing or scale of future interest rate cuts.

What this means for businesses and consumers

For businesses, rising oil prices combined with a weaker rand create immediate cost pressures. Transport and logistics companies are the most exposed because fuel represents a significant share of operating expenses.

Retailers face indirect pressure through higher supply chain and distribution costs. Even when fuel is not a direct input, logistics networks pass on higher costs through pricing adjustments. Manufacturing, mining, and agriculture also face increased input costs due to their reliance on fuel and energy systems. These pressures can reduce profit margins and delay expansion or investment decisions.

For consumers, the effects are most visible in transport and food prices. These categories make up a large portion of household spending, particularly for lower-income groups. As a result, rising fuel costs reduce disposable income and increase financial strain. Over time, sustained cost pressures can also affect wage expectations. Workers may demand higher wages to compensate for rising living costs, creating additional inflationary pressure.

Is South Africa’s economic recovery at risk?

South Africa’s economic recovery remains fragile and uneven. Growth is constrained by structural challenges, weak business confidence, and infrastructure limitations. In this environment, external shocks can have an outsized impact. Higher energy costs reduce business profitability and increase operational uncertainty. This discourages investment, particularly in sectors that depend heavily on energy inputs.

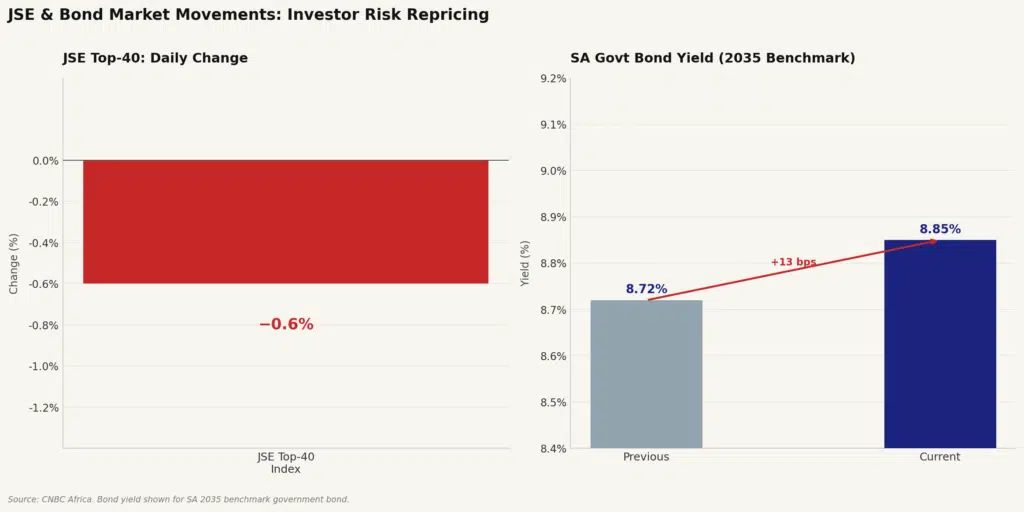

At the same time, households face higher living costs, which reduces consumption demand. Financial markets have already responded to the shift in sentiment. The Johannesburg Stock Exchange (JSE) Top-40 index fell by 0.6 percent, while government bond yields rose by 13 basis points to 8.85 percent on the 2035 benchmark.

These movements suggest that investors are pricing in higher risk and weaker growth expectations.

When equities fall and bond yields rise simultaneously, it often signals a reassessment of macroeconomic stability. Currency weakness adds another layer of pressure by increasing imported inflation risk. If oil prices remain elevated for a prolonged period, South Africa’s recovery could lose momentum. This would make it more difficult to achieve sustained growth in the medium term.

Mokoena notes that the transmission from energy shocks to growth expectations is usually indirect but persistent in South Africa’s case.

“When oil prices stay high while the rand remains under pressure, it gradually feeds into weaker confidence and delayed investment decisions across the economy,” she said.

According to her, if these conditions persist, policymakers may face a more complex balancing act between supporting growth and containing inflation pressures.

What investors and policymakers should watch next

Investors should focus on upcoming domestic economic indicators, including gross domestic product figures, mining output, manufacturing activity, and current account data. These will help determine whether domestic fundamentals are improving or weakening under external pressure.

At the global level, oil price movements remain the most important variable. Geopolitical developments in the Middle East will continue to influence energy markets and risk sentiment. US economic data and Federal Reserve policy expectations will also shape dollar strength and global capital flows.

For South Africa, the central issue remains exposure to external shocks. Currency movements, commodity cycles, and global risk sentiment will continue to drive inflation, financial markets, and growth expectations.

The current environment highlights a structural challenge rather than a temporary fluctuation. South Africa’s sensitivity to global energy and currency cycles remains a key constraint on economic stability.